Over the last few years there’s been a lot of talk about whether value investing still works. Without rehashing what the two sides are, I would argue that it’s not dead, but rather simply misunderstood, and it’s important to assess what value investing is on a first principle basis.

Say you have two businesses, company X which is highly valued at some X multiple of revenue, and a company V which is valued very cheaply at some small multiple of FCF or earnings. Over the last several years, investors may have observed that company X have enjoyed more share price growth than company V even though it looks like company X is more expensive. Some may go as far as to say value investing in companies like V simply doesn’t work anymore. I would argue this is an incorrect assumption based on faulty interpretations of recent market trends.

To assess if value investing is still alive and well, it’s important to first recognize why value investing works in the first place. The basic element of value investing is you’re buying some business that’s valued at a low Price/FCF basis which results in a good yield on your invested cash annually. This is an attractive way of investing because it offers investors a sense of confidence, in that their valuation of a business is grounded on something, and that something is real returns. The keyword here is real returns.

The problem I see with many of these ‘value’ picks today, is that while the business is generating cash, it isn’t returning it. This causes people to question if value investing works when they should really be reassessing whether the business they’ve invested in is truly returning the FCF they generate.

While many investors may have a slightly different flavor of value investing, mine is that it offers an acceptable return on my investments.

However that return of value generated by the business must be real. I would generally accept the following 3 ways of being paid back for my investments:

The business is reinvesting earnings into more (real) growth

The business is buying back stock

The business is paying a dividend

#2 and #3 are traditionally how you would be paid back, but I would argue #1 is a more attractive way of being ‘paid’ back, and also my preferred method.

The problem with many of the value stocks I see out there today is that they do not grow, they do not buy back stock, and they do not pay a dividend. At which point, I would ask the question; when am I going to be paid for my investments? The companies that do not take action to repay investors the FCF they generate are NOT value investments, they are simply retirement homes for management and board members to reap all the rewards while investors question if value investing works.

Value investing works, some investors are simply not invested in a company that is returning value to investors. Instead of questioning if value investing works, it’s important investors reassess if these ‘value’ businesses are really of high value from a first principle basis as opposed to simply looking at their multiples (are they returning their cash to you?).

I was introduced to AUTO late last year and recently got around to taking a look at this business. I was attracted to it primarily because this is a lead gen business which has many of the same qualities as SaaS businesses on their rev gen side (marketing metrics/conversion rates). AUTO acquire website traffic via their portfolio of sites, convert this traffic into leads, and sells it to local dealerships. A capital light business that have some similarities to SaaS and tech businesses we’re normally invested in. Ultimately I decided against taking any positions, but I thought I’d share my quick analysis of AUTO with those who are interested. Feedback is welcome if I missed anything as I may take another look at it in the future.

AUTO is a lead gen business that owns a portfolio of automobile related websites, namely: autobytel.com, car.com, usedcars.com, and usedtrucks.com.

This is a an asset and capex light business in that they generate traffic from different sources (which I’ll cover briefly below), convert these traffic into leads of customers who are interested in used cars, and then sell these leads to local dealerships who has the inventory of the cars customers want. In a general sense, AUTO’s business makes sense and provides value for both their partners (car buyers and car sellers).

I’ll spare everyone the history of the business, but the short version is the old management team was shown the door due to poor management and declining revenues. New CEO was brought in and brought in his own executive team in 2019.

When the old guards leave and new ones come into a declining business, investors want to see the following:

Transparency, and honesty on how the business is actually performing (PAR’s new CEO is a great example of how a new CEO should act)

A plan to get the business back on track

Signs that the business is stabilizing

Unfortunately I would rate management’s #1 & #2 as a 5/10 at best, and as for #3, there’s been no signs the business decline is stabilizing.

#1 & #2: After joining, the new management’s plan is essentially optimizing on revenue per lead as opposed to driving new leads. This is very disappointing as it shows management has no plan to solve the root cause of their problem to begin with, which was the decline in traffic (i.e., revenue).

I’m equally disappointed in the constant frugality talk instead of solving their root problem. “What you’ll find is that we are doing more with what we have” (19Q3 CC)

Most of the company’s trouble have to do with a decline in traffic and unfortunate timing in the slowdown of the US auto market. AUTO lost many of their paying car dealerships in the last 2 years in the market wide slowdown. However this is conflicting, as when car sales drop, you would think car dealerships would be more inclined to buy qualifying leads.

This leads me to believe car dealerships do not find AUTO’s leads meaningful in providing a ROI, and dealerships are cutting cost around ineffective marketing (AUTO’s leads) and increasing spend elsewhere (Google Ads). Indeed, management have also signaled in conference calls that they have been revamping their internal tracking systems to better show ROI for dealerships. I believe until this problem is solved and dealerships are persuaded that they should be spending their marketing dollars with AUTO, AUTO will continue to experience difficulties keeping old clients and signing new ones.

#2 and #3: As mentioned earlier, I was initially attracted to AUTO’s business model frankly because the same rev gen models that are used to calculate conversion rates from SaaS or growth tech companies can also be used with AUTO. At it’s root, AUTO can sell more leads if it can generate more leads, and if it can generate more leads if it gets more traffic. However the decline of their traffic have resulted in a decline in revenue, and new management is currently optimizing this remaining traffic instead of growing their traffic base.

While optimizing their conversion rates is a understandable thing to do, you’ll never grow if you’re forced to make more with the same amount. You don’t get rich by trying to make the most of a minimum wage job, you get rich by making more money (while also optimizing your monthly spend).

It’s admirable that the new management is looking to stabilize the business by increasing conversion rates and optimizing lead revenue, but this doesn’t fundamentally change their situation until they can find a way to renew their lost traffic. The current optimization plans will at best get them to a rough breakeven point. Their current market cap is 30M, with a 1.1M balance sheet while losing 2M per quarter. While they can likely bring in some AR, this will likely only buy them a longer runway until they can solve the real problem.

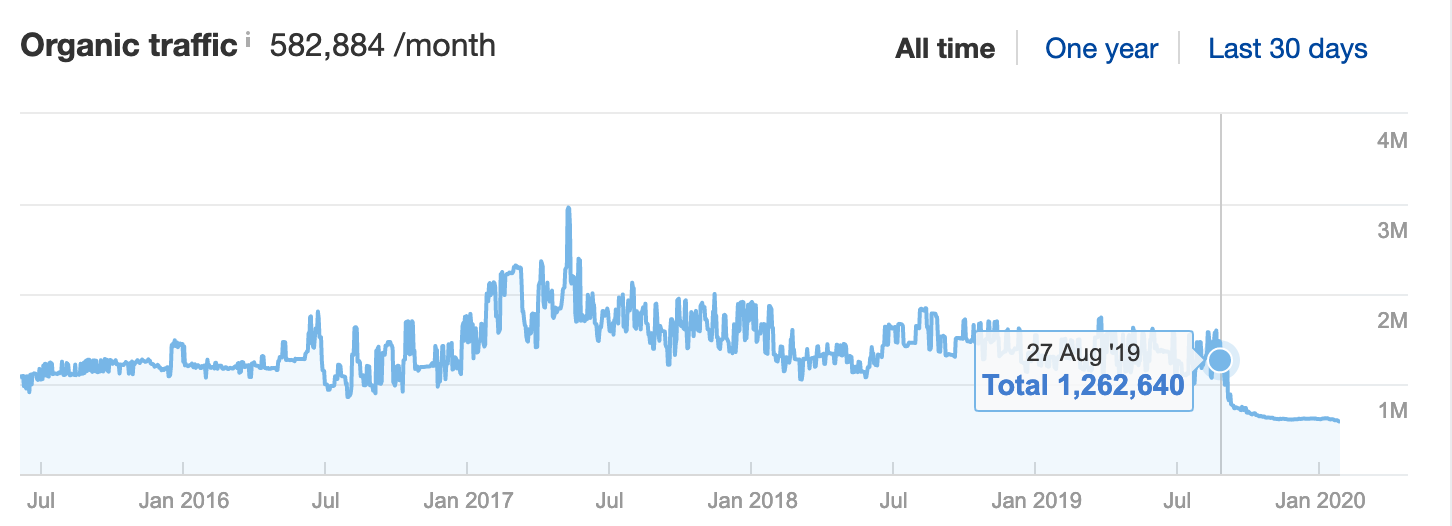

Importantly, we noticed AUTO’s primary website Autobytel.com’s traffic halved in late August 2019, dropping from an average of 1.2M visitors per month, to 600k per month:

Source: Ahrefs.com

With Q4 2019 earnings coming up, AUTO will likely be reporting more bad news before any good ones come in.

For now, I’ll be waiting on the sidelines until they can prove they have a plan to increase traffic and revenue, show stabilization in quarterly losses, and importantly show some honesty in their performance metrics.

To receive more ideas like this, subscribe to our mailing list:

It’s finally 2020. Over the holidays I recalled a conversion I had with a colleague where in early 2019 we spoke about the results of the Q1 2019 CFO Survey, which had the headline “Recession Expected by Late 2020” and stated that “Sixty-seven percent of U.S. CFOs believe that the U.S. will be in recession by the third quarter of 2020, and 84 percent believe that a recession will have begun by the first quarter of 2021.” I felt this was meaningful as the CFO Survey results are aggregate of around 500 CFOs based in North America, so it had some representation of what CFOs think.

As it’s now Q1 2020, I felt it’s only fitting to go back to check up on the results of the survey over the course of the year and see how their predictions changed over time, here they are:

There’s a few interesting observations. First, at least half of CFOs believe a recession is just around the corner (6-9 months out), while the significant majority (70-80%) believe a recession will happen within 12 – 24 months. Second, it seems these timelines gets postponed a little quarter. Most like the dangling a carrot in front of the horse.

One thing to note however, and this seems evident in the fund manager circle as well, is that a good number of people seem to think there’s some market risks around the mid-2020 election time frame, and to an extent, increased market volatility. The CFO survey results is also consistent in this regard, having a recession expectation around this time frame in each of their last 4 survey results.

The other thing that’s been going around is that it seems most firms predicts 2020 to enjoy some modest stock growth based on what ever reason they choose to use this time. So to summarize, it seems census believes:

Market risk around US elections

Increased market volatility

Modest market growth

For the most part I think these predictions are pretty reasonable. I think the folks who are buying utilities to be more defensive are taking it a tad too extreme (I also believe utilities are over priced at the moment, but that’s a separate post). I don’t think 2020 will be too bad, but it may be painful for some. I don’t think 2020 will be too great, but we’ll likely see modest gains across the market.

In terms of portfolio strategy for 2020, we are likely to raise cash while reduce holdings in stocks with the lowest expected returns (the least favourite of our favourites), as well as stocks that require the longest timelines to play out. We are also likely to sell into highs and buy lows, consistent with our belief that we’ll see some volatility (opportunity) and overall market gain for 2020.

Also, if volatility increases meaningfully, we’re likely to write options around our favourite names.

I wanted to do a very quick

review of SMSI as it’s share price have dropped meaningfully since my last

write-up with no fundamental change for it’s business, and I believe it now

offers an extremely attractive price for a growing software business.

I covered SMSI in a recent blog post prior to their Q2 earnings. At

the time SMSI was trading at $3.20/share (May 25, 2019). Shortly after Q2,

their stock doubled on strong earnings report but have since pulled back after

Q3’s earning report on no great reasons. I believe this is a once in a blue

moon opportunity to buy into a robust recurring revenue generator growing at

FAANG speeds (40%/yr) while at an extremely attractive price.

This will be a quick update note as a couple things have

changed in favor of investors over the last few months.

A brief Intro of

SMSI:

SMSI has 3 primary products (apps):

SafePath: an app that comes in 3 different set of functionalities. SafePath

Family is a set of features that allow it to control, connect and track other

phones with the app installed, primarily marketed as a family safety app, very

similar to Apple’s “Where’s my phone” app, but with more features which I won’t

cover here. The second and 3rd set of functionalities (SafePath IoT

& SafePath Home) allows this app to control and connect to other devices

like trackers, smart watches, security cams, etc. If you’ve used the Google

Home app, SafePath works in a similar way (although with a different UX and more

features). Between SafePath Family, Home, and IoT (all 1 app, just marketed as

3 separate feature sets) SMSI positions this app as a single device management

app that allows users to connect and control smart devices they have around

them (phones, trackers, cameras, TVs, etc). SMSI sells this app via partnerships

with major MSO and carriers, who then resells this app as a rebranded white-label

product to their own phone subscribers. I.e., SMSI partners with Sprint, who

then sells this app to Sprint’s customers. Sprint charges 7/month, they split

the revenue.

Commsuite: a voice to text app, but with more features but

again I won’t cover those here, basically work similarly to Google Voice. Also

sold via carrier & MSO partnerships to these carrier’s end customers, just

like SafePath. Both Commsuite and SafePath obtains MRR as they’re subscription

services like Netflix.

ViewSpot: a new app SMSI acquired last year. It allows you

to configure a phone to only show specific content (a sandbox). If you’ve ever

had the unfortunate experience of turning on your Windows laptop in “safe mode”,

this is similar to it. This app is sold to retailers and carriers and used by

these retailers and carriers as a sales agent. Carriers install this sandbox app

on their display phones and tablets with pre-configured content (like the display

phone’s key features, pricing, etc) primarily to help sell the display phone.

SMSI receives recurring subscription revenue from their carrier customers based

on the number of stores with this app installed. SMSI also receives additional ‘campaign’

revenue whenever carriers launch a new phone (i.e., IPhone 11) in their stores

(think of ‘campaign’ revenue as a form of professional services).

This is a brief overview and I would encourage those

interested in SMSI to understand their products in more detail. The short

version is SMSI is application developer (industry: pre-packaged software) that

sells it’s products to carriers to form marketing channels, these carrier

partners then help them market and sell these products and they split the

revenue. SMSI’s products are white-labeled for the carrier and acts as a

revenue center for the carriers, while SMSI focuses on updating and building

out the feature set of these products.

As I mentioned this is meant to be a quick update so I’ll skip to the more relevant things. SMSI had a blow out quarter In Q2 of 2019, finally turning massively profitable as I had anticipated and the share price doubled in the subsequent weeks.

After Q3 however, SMSI’s prices dropped by 40%. Nothing

fundamentally changed for the company, but I believe this selloff was primarily

due to the pending merger between Sprint and T-Mobile (more on this below). The

TMUS & S merger has been in the works over the last 2 years so this shouldn’t

be news, but given the state attorney’s trials it’s understandable that

investors view this as a risk factor.

Sprint & T-Mobile Merger

This story impacts SMSI primarily because Sprint accounts

for 77% of SMSI’s revenues, and following the “merger” (acquisition) T-Mobile

will become the operating entity. If this looks worrisome, don’t be, much like

my late grandmother’s pies, it looks much worse than it actually is.

Around the summer of 2018 SMSI’s management team begun

guiding towards a pending Tier 1 carrier signing. At the same time, T-Mobile

and Sprint announced their merger plans. SMSI’s management continued to guide

toward this T1 carrier partner in the subsequent quarterly conference calls. It

was widely expected that the T1 carrier would be T-Mobile. Our channel checks

had also confirmed this would be the case.

However in Q3 2019 (prior to the stock price drop), SMSI’s

management weakened their guidance to:

“It remains true that there is always risk with M&A

activities, due to a variety of unknowns and things out of our control.

However, we also see an equally great opportunity for growth and expansion of

our business case as well.“

This was weakened from the previously guided T1 pending customer. The stock dropped in the following 3 months, worsened by end of year tax loss harvesting. I believe this drop is overblown. The weakening of SMSI’s guidance was immediately following the same time frame as the 2019 State attorney general lawsuit to block the TMUS & Sprint merger.

I believe while they’ve had to tone down their guidance on conference calls publicly, nothing fundamentally changed and they are still ramping up in anticipation of the T-Mobile signing. In fact, SMSI’s management has been on a significant hiring ramp the entire year, increasing their headcount from ~160 to ~200 as of Dec 2019. Actions speak louder than public guidance.

Separately, SMSI’s management have said that nothing have

changed in regards to the T1 signing and their teams have been working with the

merger teams at T-Mobile and Sprint directly. You can’t ask for much more ‘color’

than that.

Operating Model

The Q3 selloff is overblown and the subsequent tax loss

harvesting have worsened the share price decline. I believe this is a once in a

blue moon opportunity to buy extremely cheap shares of SMSI ahead of the

upcoming TMUS and S merger trial conclusion. Numerous channel checks at TMUS

and Sprint’s other vendors have point to a Feb – March timeline on new deal

signings following the Jan 15 trial conclusion date.

SMSI is a 150M market cap business with 24M in cash,

generating 5M and growing per quarter with no debt. We’re basically buying the

business for 125M that generated 11M in cash this year and will generate 25M in

2020 and 41M in 2021. 2020 and 2021 earnings based on CFO guidance and assumes

zero new carrier wins (not pricing in T-Mobile).

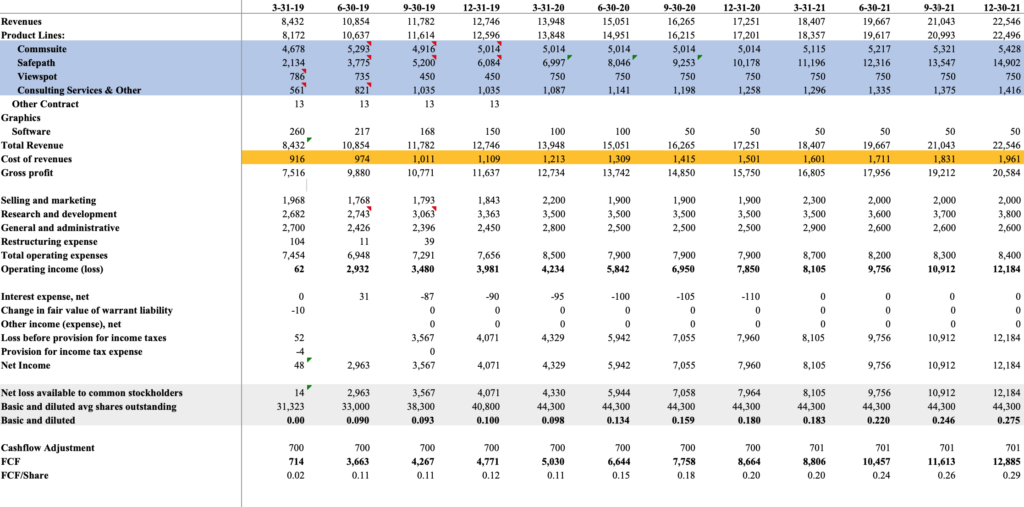

My updated model for SMSI reflects the guidance CFO Tim

Huffmyer provided, which was recently reaffirmed:

SMSI Operating Model

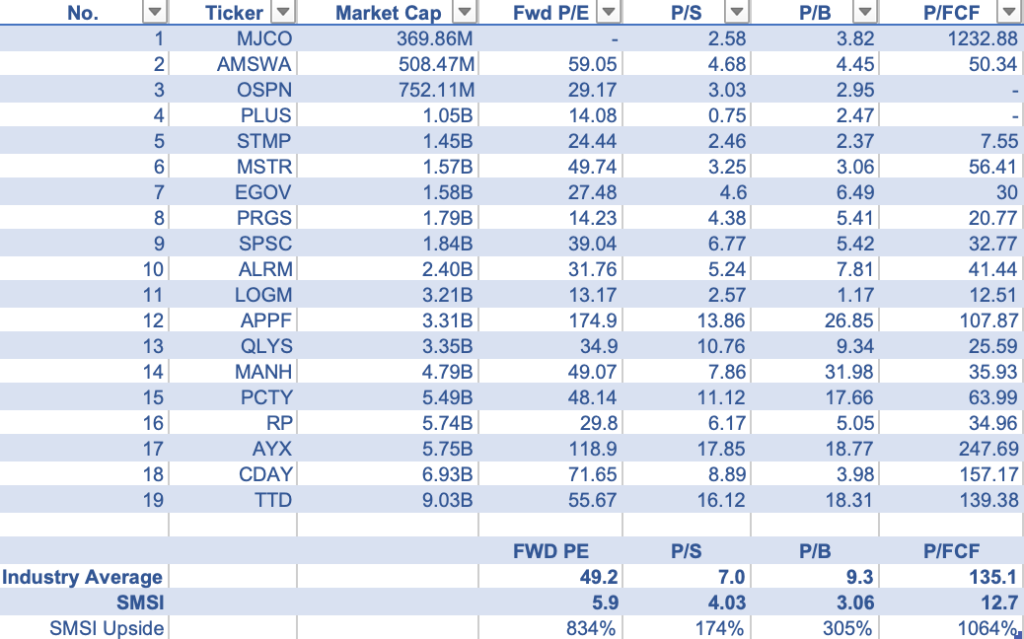

Valuation

I think SMSI is cheap on a FCF basis (2020 P/FCF of under 6),

but some prefers to relative valuations, here is SMSI against its industry

peers:

SMSI valuation compared to pre-packaged software industry peers.

Conclusion

I believe the recent selloff is due to the softening of TMUS

& Sprint merger guidance management provided on Q3, worsened by end of year

tax loss harvesting. However, management actions and channel checks reaffirm T1

signing by early next year. SMSI is extremely cheap even assuming no T1 signing

with TMUS. With the likely Russell 2000 inclusion, and T1 signing in early to

mid 2020, SMSI shares will likely be a multi bagger in within 12 months.

Disclosure: I own shares of SMSI and call options. Published as of Dec 27, 2019.

I feel like it’s a good time to talk a bit about global macro economics given the recent change in the direction of the US-China trade deal and news in the weakness of US Q1 GDP numbers.

I have to caveat this by saying I’m a stock picker that buys great valued businesses at fair prices and I’m no expert in economics. Although admittedly the excitement in macro economics do influence my decision on the positioning and hedge of my investments.

Currently the portfolio is nearly fully hedged against downturns via put options on the Russel 1000 Value Index (IWD). I would have preferred hedging against IWC, however liquidity is low on IWC and I place a higher value on options liquidity in the event I wanted to pull back on the hedge at reasonable prices.

My hedge against market downturn will say a lot about my thinking around my macro view.

I would ideally like to stay invested in the market as long as possible, while appreciating the fact that eventually (and I don’t know when) the market would likely drop. Economists have been predicting a downturn since the 2016 scare and if anybody listened to them, they’d lost out on a lot of money.

I won’t repeat what’s happened with the trade war, except to say that it’s taken a turn for the worst. I do believe a trade deal could happen. However I’m not betting on it and feel obligated to hedge against the increasing downside risk we’re seeing in the global investment environment.

The short version of it all is that Trump is moving forward with more tariffs in light of China backing out of their prior agreements. Q1 US GDP numbers were higher due to businesses preempting the trade war tariff impacts, and not actual strength in the economy. Now that this is evident, the Atlantic Fed’s GDP NOW and others have all revised down Q2 GDP numbers from ~2.5 to ~1-1.5 annualized.

A recent report by the CFO Survey provided fairly interesting tidbits. I find this survey to be a bit more meaningful than what economists think simply due to the fact that CFOs, who’s jobs are to allocate a business’s capital, should have a better handle on where and when to put their capital to use; and this should be an early indicator of GDP growth (at least the business investment component of it). I will mention that if you look into the raw data, their number of respondents is actually fairly low and I would hesitate to place too much weight into the survey results. FYI.

If you were to believe the result findings, then the US is expected to enter a recession in late 2020 / early 2021. The 1Q19 release basically says 67% of CFOs believe we’ll enter a recession in the next 16 months, with that number up to 84% by early 2021, while sentiment have dropped in 2019.

I have been fairly cautious since early 2018 but have stayed nearly fully invested for the entire duration mainly because I have no clue when the next recession will happen, and if we invested like a recession is always around the corner, than our returns would suffer greatly. This is not to say you should be aggressive in your positioning, it’s just that when I don’t know what’s going to happen to geopolitics or global economics, i stick to what I do know; stock picking. However I am of the belief that there’s a bit of a self fulfilling prophecy in the fact that when business leaders believe a downturn will occur, it impacts their investment sentiments and how they run their businesses, which in turn may impact the actual economy.

How this al impact my investment plan is basically as follows: I plan on raising cash in the next 6-12 month while lowering our market hedge. Cash is the best thing to hold in anticipation of any downturn, and I plan to raise our cash holding up to a more modest level in the short term.

I may provide an update on my macro view in the next few months however I hesitate to provide it too often. The Real Economy doesn’t change as fast as the news cycle nor politicians with their rhetoric. In the meantime, I’ll stick to looking for good businesses to buy.